Top 10 Saving Tips for Beginners

Saving money can feel overwhelming, especially when you’re just starting out. But don’t worry—you’re not alone. Many face challenges balancing budgets, managing unexpected expenses, and avoiding impulse purchases. According to Forbes, only 39% of Americans have enough savings to cover a $1,000 emergency expense, highlighting the importance of financial preparedness. This guide offers practical, easy-to-follow tips to help you save money effectively and build a strong foundation for financial security.

Let’s embark on this journey together, focusing on understanding and actionable insights. We’ve got this, one step at a time.

1. Establish a Realistic Budget

Creating a budget is the cornerstone of effective money management. Begin by itemizing all your sources of income and expenses. Divide your expenses into fixed costs (such as rent and utilities) and variable costs (such as groceries and entertainment). For a detailed understanding, check out your article here to learn about the essential components of a budget. This guide will break down complex concepts into simple, actionable steps, helping you overcome common challenges and misconceptions about budgeting.

A well-crafted budget is a powerful tool for achieving financial success:

- Track Your Spending: Use budgeting apps to monitor your spending habits closely. This will help you understand where your money goes and identify areas for improvement.

- Set Limits: Allocate specific amounts for each spending category and stick to them. This ensures you stay within your budget and avoid overspending.

- Review Regularly: Take time each month to review your budget thoroughly. Adjust as needed to reflect any changes in your financial situation. This keeps your budget relevant and effective.

Remember, budgeting isn’t just a one-time task; it’s an ongoing process of monitoring and adjusting. Stay committed and patient! Mastering your budget is essential for achieving long-term financial stability.

2. Prioritize an Emergency Fund

An emergency fund is a crucial financial safety net for unforeseen expenses such as medical bills or car repairs. While you should save enough to cover three to six months’ living expenses, the key is consistent saving, regardless of the amount. Every contribution accumulates over time.

For a more in-depth understanding of its importance, I invite you to read my article, “Emergency Fund Rule,” which explores this topic further.

Tips for Building Your Emergency Fund:

- Start Small: Initiate your savings with a low target, such as $500, and gradually increase this amount.

- Automate Savings: Establish automatic transfers to your savings account to ensure consistent contributions.

- Keep It Accessible: Place your emergency fund in a high-yield savings account for easy and immediate access.

By following these steps, you can establish a robust emergency fund that ensures financial security and peace of mind.

3. Automate Your Savings

Automating your savings ensures consistency and reduces the temptation to spend. A common misconception is that you need a lot of extra money to make automation worthwhile. In reality, even small, regular contributions can add up over time and make a significant difference in your financial health.

Tips for Automating Savings:

- Small, Consistent Transfers: Even saving a few dollars weekly can lead to significant accumulation over time. Set up automatic transfers from your checking account to your savings account for an amount you are comfortable with. This straightforward approach can have a substantial impact on your long-term savings.

- Leverage Simple Savings Tools: Use applications that round up your daily purchases to the nearest dollar and save the change. These tools offer a hassle-free method of saving small amounts regularly, making the process of saving seamless and stress-free.

By incorporating these strategies, you can gradually build a financial cushion without feeling overwhelmed. Each small action contributes to your larger financial goals. Consistent and deliberate savings practices are crucial to achieving economic stability and success.

4. Cut Down on Debt

High-interest debt can significantly hinder your ability to save money. However, effective strategies exist to manage and reduce this type of debt. You can make substantial progress in your financial journey by implementing strategies to manage and minimize high-interest debt.

Strategies to Manage and Reduce High-Interest Debt:

- Snowball Method: Begin by eliminating your smallest debts first. This tactic helps to build momentum and maintain motivation throughout your debt repayment journey. Even small victories can provide the encouragement needed to keep moving forward.

- Avalanche Method: Initially, prioritize paying off debts with the highest interest rates. Over time, this method can reduce the total amount of interest paid, resulting in more savings. If funds are tight, focus on paying just a bit more than the minimum on these high-interest debts to gradually reduce them.

- Debt Consolidation: Evaluate the option of consolidating your debts to obtain lower interest rates, making your monthly payments more manageable and streamlined. Exploring community resources, credit unions, or non-profit organizations offering free financial counseling can be valuable in finding consolidation options.

Managing debt is a journey; each step gets you closer to financial freedom. Stay patient and consistent—these are your best allies in untangling the complexities of debt repayment.

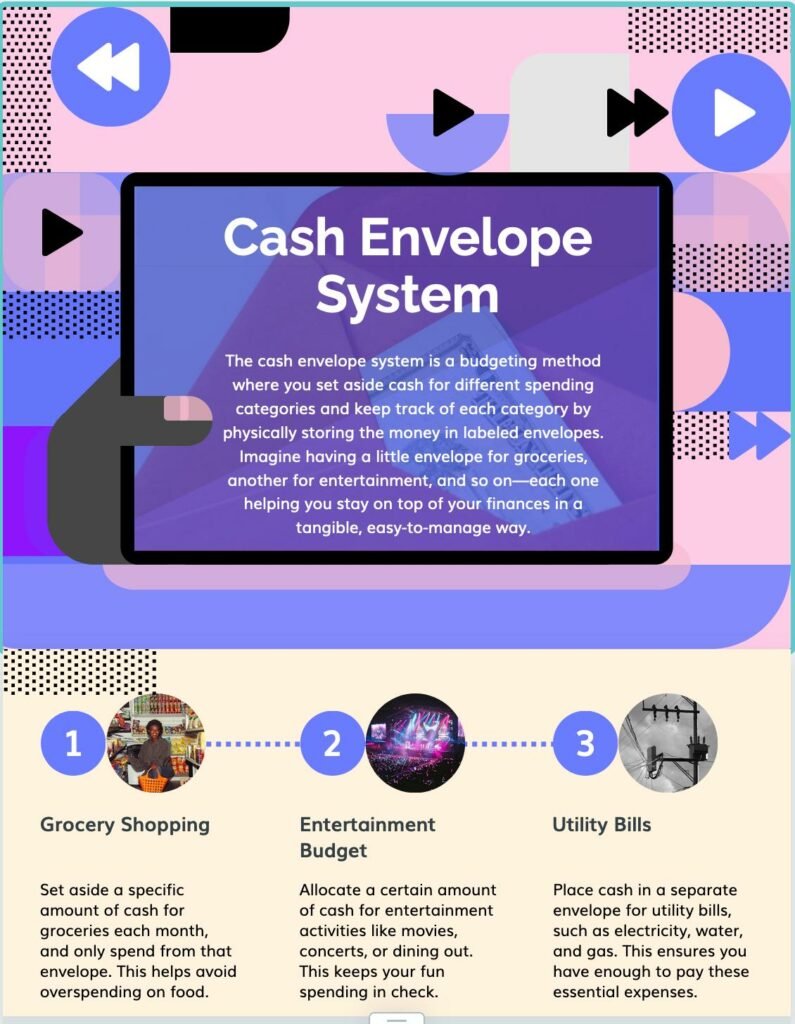

5. Utilize Cash Envelopes for Discretionary Spending

The cash envelope system is an easy and effective way to budget. This approach involves setting aside specific amounts of cash for different spending categories like groceries and entertainment. By using physical cash instead of digital transactions, this method provides a more tangible approach to budgeting, enabling you to manage your spending more effectively. By using cash, individuals can better manage their finances, ensuring they stay within their budgetary limits and avoid overspending. This system fosters a disciplined approach to financial management, making it an accessible tool for anyone looking to improve their budgeting skills.

Tips for Using the Cash Envelope System:

- Set Limits: Decide on a specific amount of cash for each necessity, such as food and utilities. This will help you visualize and control your spending.

- Maintain Discipline: When the cash runs out, you’ve hit your spending limit for that category. This approach promotes mindful spending and helps prevent overspending.

- Review: At the end of each week or month, evaluate your spending habits and adjust your envelopes as needed. This ongoing review ensures your budgeting system evolves with your financial needs and goals. By regularly assessing and refining your approach, you can maintain an effective and adaptive financial strategy.

By breaking down spending into manageable segments, you gain control over your finances, fostering a healthier, more sustainable money management approach. This method offers a clear, disciplined framework for effectively managing your financial resources, no matter your budget size.

6. Shop Smart and Save

A study conducted by CouponFollow in 2021 reveals that the average American household could save up to $1,465 annually by utilizing online coupons. By adopting smart shopping practices, individuals can significantly enhance their financial savings.

Top Tips for Smart Shopping:

- Seek Promo Codes: Identifying and utilizing promo codes can result in significant savings on your purchases. As SimplyCodes highlights, online coupons can save you an average of $30 at checkout, cutting your total spending by 17.2%.

- Compare Prices: Always check prices on different websites to find the best deal before buying.

- Buy in Bulk: For items that don’t spoil, purchasing in bulk can save you a lot of money in the long run.

Implementing these methods can significantly enhance your strategic and effective shopping habits, improving your financial well-being. By integrating these practices, you are positioning yourself to make informed, thoughtful decisions that contribute to long-term financial stability.

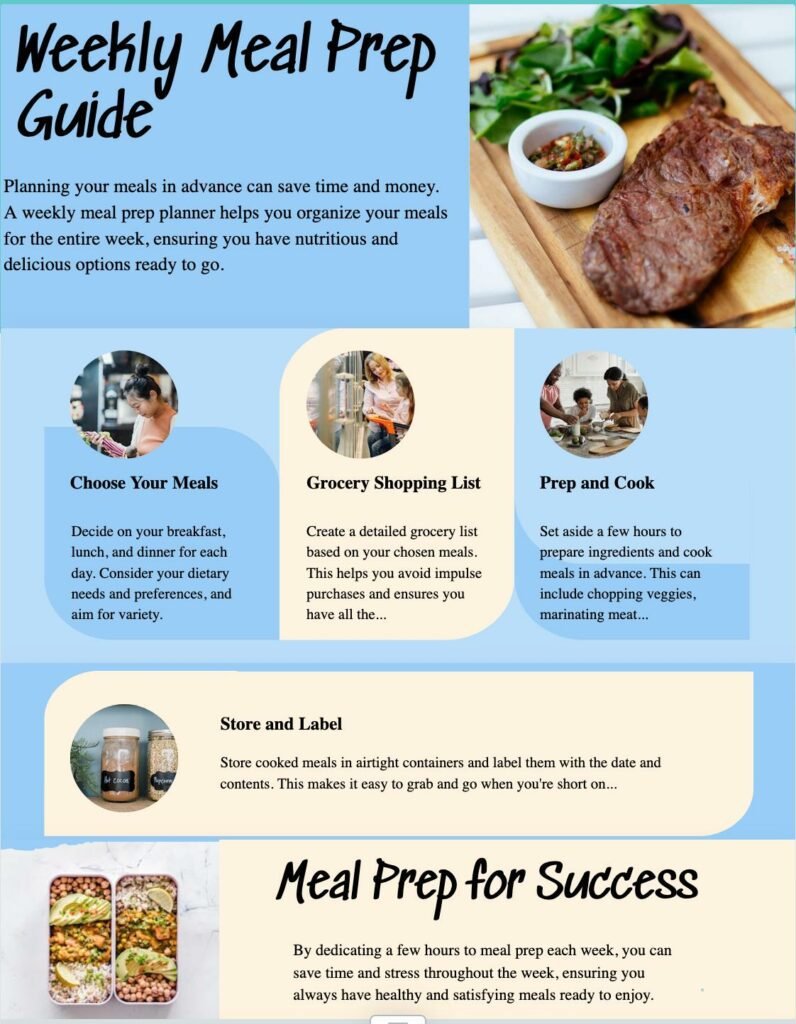

7. Cook at Home and Meal Prep

Eating out a lot can really hit your wallet hard. Cooking at home and prepping meals can save you a ton of money while helping you eat healthier. It’s a win-win for your budget and your long-term health.

Winning Strategies for Meal Prepping:

- Plan Your Meals: Kick off with a weekly meal plan and grocery list. This crucial first step keeps you organized and on track.

- Batch Cooking: Cook in bulk and store meals for the week. This not only saves you precious time but also ensures you have nutritious options ready to go. Plus, it’s a smart way to save money. According to Barclays, 29% of shoppers batch cook to cut down on grocery expenses.

- Utilize Leftovers: Get creative with leftovers to minimize food waste. It’s good for your wallet and the planet.

By following these steps, you will be well-prepared to navigate your financial journey with confidence and clarity.

9. Take Advantage of Employer Benefits

Maximizing your savings can be straightforward by fully utilizing the benefits your employer offers, such as retirement plans and health savings accounts (HSAs).

Here are some actionable steps to consider:

- 401(k) Match: Ensure you contribute enough to receive the full employer match. This adds extra funds to your retirement savings at no additional cost.

- Health Savings Account (HSA): Utilize an HSA for tax-advantaged savings on medical expenses. This approach effectively manages healthcare costs while also preparing for future needs.

- Flexible Spending Account (FSA): Using an FSA lets you save on taxes for out-of-pocket medical, dental, and dependent care expenses. This financial tool can help you manage everyday costs more effectively, ensuring a more organized approach to your financial well-being.

Following these steps can simplify your financial planning and set you on the path to greater financial security. Remember, effective financial management means maximizing the resources at your disposal.

10. Educate Yourself on Personal Finance

Knowledge is power, and understanding personal finance is crucial for managing your money and making informed decisions. A recent Experian survey reveals that three out of five adults believe their limited knowledge of credit and personal finance has led to costly mistakes. A startling 60% of these individuals reported losses exceeding $1,000 due to these errors. This statistic highlights the critical need for personal finance education to prevent costly mistakes.

Here’s how you can start:

- Attend Free Workshops: Look for free financial education workshops in your community or online. Local non-profits and community centers often host these sessions and offer valuable resources.

- Follow Financial Podcasts: Listen to podcasts dedicated to personal finance tips, especially those designed for beginners. These podcasts provide practical advice that you can implement immediately.

- Utilize Public Resources: Leverage the free resources available at your local library. Many libraries provide access to financial planning books, magazines, and online courses at no cost.

Get the tools and know-how you need to take control of your finances and smash your financial goals with confidence—master budgeting, saving, and investing to build a rock-solid financial future.

Key Takeaways

Saving money doesn’t have to be daunting. By following these practical tips, you can start building a secure financial future and unlock endless opportunities through financial literacy. Here are the key points covered in this article:

- Create a Budget: Keep track of your income and expenses to understand where your money goes. A well-structured budget helps manage your finances efficiently and can reveal areas where you can cut unnecessary spending.

- Set Savings Goals: Whether for an emergency fund, retirement, or a dream vacation, having clear goals motivates you to save. Start with small, achievable targets and build from there.

- Automate Savings: Set up automatic transfers from your checking to your savings account. This ensures you save consistently without even thinking about it.

- Reduce Debt: High-interest debt can hinder your savings goals. Focus on paying it down to free up more money for saving.

- Cut Unnecessary Expenses: Analyze your spending and find areas to cut back, like dining out less or canceling unused subscriptions.

- Embrace a Frugal Lifestyle: Live within your means by shopping sales, using coupons, or buying second-hand items.

- Invest Wisely: Understand your investment options and put your money to work. Diversifying your investments can yield better returns over time.

Remember, financial literacy is the key to unlocking a world of opportunities. Join my mailing list to be the first to know when new blog posts drop! Stay informed to make smarter financial decisions. Happy learning!

Feel free to share your stories on how these tips have helped you by emailing us at hello@themisfitfinance.com.